Fundraising in a shifting market

Industry leaders gathered at the Bank of America Triangle Innovation Summit to discuss how founders can thrive amid capital constraints and AI disruption.

4 minute read

Key takeaways

- Even with record amounts of uninvested capital, many VCs, LPs and startups looking for deals are stuck in a holding pattern.

- Attention is shifting from companies building AI platforms to those deploying AI throughout their operations.

- Prospective investors are looking for capital efficiency, companies in niche markets, and curious, open-minded management teams.

Navigating a new VC and PE landscape

The private capital markets have been on a rollercoaster ride since the pandemic began —falling, then sky-high, then resetting and then, in early 2025, full of anticipation that the next wave of AI and potential fiscal tailwinds would unleash pent-up demand. But despite a record amount of dry powder, or uninvested capital, persistently higher interest rates combined with global economic instability have left many VCs, LPs and startups wary and stuck in a holding pattern.

Add to that the increasing dominance of AI in all conversations, and those investors and startups looking for deals are recalibrating their expectations — and working to find new ways forward.

For many startups, longer paths to liquidity are the new norm. Unable to field an IPO or a new round of funding, many maturing startups are taking longer to exit and are pursuing alternate financing methods to extend their runway. “At the pre-seed and seed stage, the average hold time for an investment is now pushing eight-plus years. The average marriage in the U.S. is shorter than that,” said Mahati Sridhar, a partner at Revolution’s Rise of the Rest. “We have seen a lot of pre-empted rounds, rounds not even going to market. We’re seeing more insider bridge rounds. These companies are kind of tweeners; they're in between rounds. They haven't really hit those key milestones, and they're relying on their existing cap table to come in and put in a little bit more capital into the business to help them get to those milestones, to kind of nudge them forward.”

“At the pre-seed and seed stage, the average hold time for an investment is now pushing eight-plus years. The average marriage in the U.S. is shorter than that.”

Meanwhile, competition for investor attention is intense. In this hypercompetitive environment, it’s no longer about doing one thing really well; a small number of diversified companies are raising billions of dollars.

David Spitz, managing director for Vista Equity Partners, put it plainly: “It’s definitely still a market of haves and have nots, given AI and the crazy multiples given to tech companies. But I believe the vast majority of companies out there are fairly reasonably valued. That wasn’t the case in 2021 and 2022 when capital was largely free.”

AI’s outsized influence

All roads seem to lead back to AI these days. Its gravitational pull is felt everywhere, and the panelists agreed the discussion is quickly “moving up the tech stack.” Although there has been a hyper-focus on the handful of companies building AI platforms, attention increasingly is shifting to companies deploying AI throughout their operations.

“It’s not just about using AI to drive operational efficiency,” said Spitz, “although I think there's a huge amount of opportunity there. That's probably already table stakes. The question is, what are you doing in your products to leverage AI, to drive value add for customers, to drive innovation? What's your data advantage?”

“It’s not just about using AI to drive operational efficiency. The question is, what are you doing in your products to leverage AI, to drive value add for customers, to drive innovation?”

Sridhar shared a snapshot from her team’s pipeline: Of the preceding 30 days of her firm’s meetings with prospective investments, she said, “One hundred percent of them mentioned AI or AI integrations.” More interestingly, 60% of those companies didn’t define themselves as an AI business. “Everyone has to leverage AI in some way, shape or form, otherwise you are going to be left tremendously behind,” she said. “But that doesn't necessarily mean you have to be an AI business.”

Concentration in the fundraising market

The panel also called out a concentration of resources — on the AI playing field, in the stock market and among venture capital firms. The “Magnificent 7” this year surpassed 30% of the S&P 500’s total market capitalization. “This whole concentration theme is warping the markets in, I think, mostly bad ways,” said Gene Riechers, venture partner of Sands Capital.

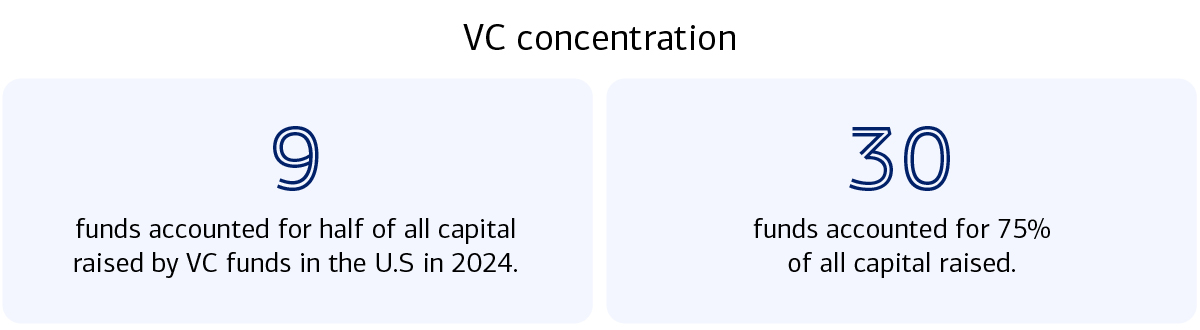

Venture capital has observed similar concentration trends. In 2024, nine funds raised $35 billion, or half of all capital raised by VC funds in the U.S.; and 30 funds accounted for 75% of all capital raised, according to PitchBook. The size of those firms has skewed the fundraising market. This shifting dynamic has had ripple effects, including on how these funds operate and deploy capital. Said Riechers, “They'll have rules like, we have to put in at least $30 million but we can't be more than 10% of a fund, okay? Well, they can't invest in a fund under $300 million. And there's lots of firms that are operating with formulas like that."

How to navigate your next raise

Given this challenging scenario, how can startups and founders position themselves for success in fundraising? What do these prospective investors look for in a founder, in someone to partner with?

Keep an eye on the balance sheet: Said Sridhar, “We really value the scrappiness and the revenue and the cash savviness that we have seen in so many of our founders to date. We want that to be a theme that continues to carry forward.” Agreed Spitz: “The thing that never goes out of style is capital efficiency.”

Focus on your niche: “All of you as entrepreneurs, try to find a niche in your market, at least a niche to get started in. You're trying to find that narrow opportunity where you can build a bigger company. We think the same way; we want to invest in entrepreneurs and teams that are focused on a very specific niche, and ideally, it's one that we know a lot about and a lot of other people don't know a lot about,” said Riechers. “What we really want to see in entrepreneurs is domain knowledge you have, or you're going to have somebody join your team who has knowledge selling to that domain. It could be a use case, it could be a vertical market.”

Try to find a niche in your market, at least a niche to get started in. You're trying to find that narrow opportunity where you can build a bigger company.”

Keep an open mind — and be flexible: “We tend to attract founders who want to learn. They've got a great company, great growth engine, they're a leader in their space, but they know they can run a lot more efficiently. They want to get double, triple their size, and they want to participate in the next part of the value creation journey. We work best with founders, and management teams in general, who are curious, open-minded, who are willing to try different things.”

One final piece of advice from the panelists: Capital formation is cyclical. Whether the dot.com bubble or the financial crisis or the pandemic or the SaaS market high of the early 20-teens, over and over the market has proved it is cyclical. When times are good, companies should raise capital and take advantage of that.

Bank of America Triangle Innovation Summit

Insights from a gathering of industry leaders and trailblazers in North Carolina’s Research Triangle.