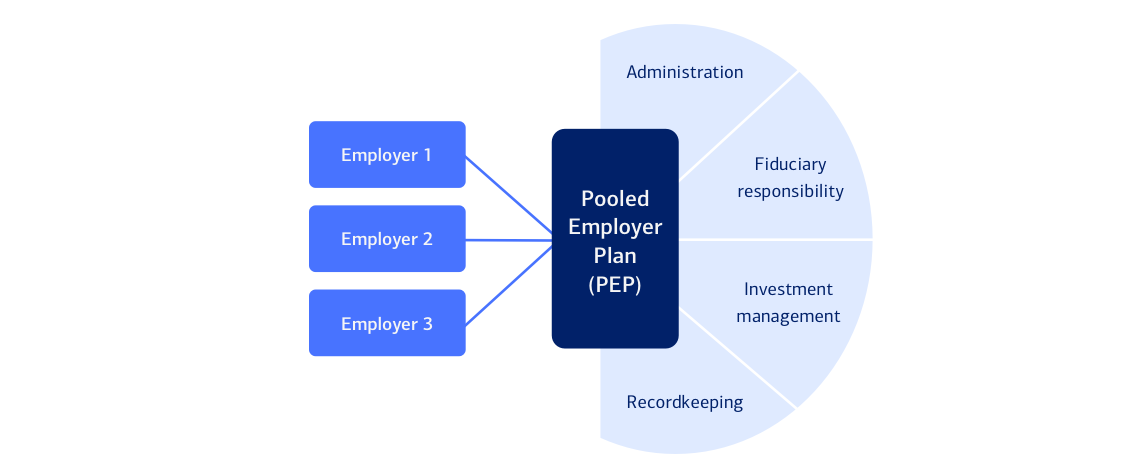

What is a Pooled Employer Plan (PEP)?

A PEP is a defined contribution plan that allows multiple, unrelated employers to participate in a single plan instead of sponsoring their own 401(k) plans. That means individual employers don’t have to carry the full responsibility for plan administration and compliance.

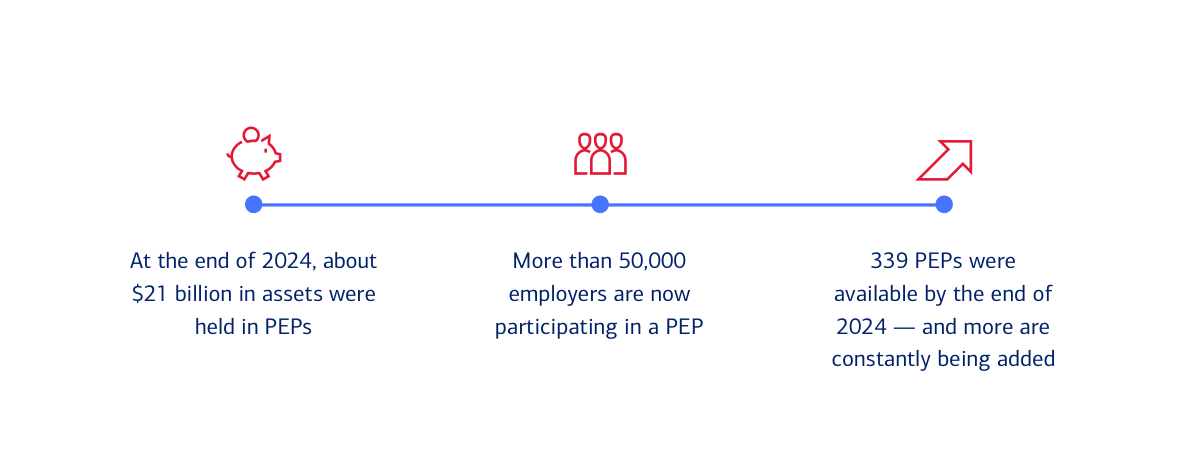

PEPs are growing in popularity

The number of participants with balances in PEPs increased 49% from 2023 to 2024.1 And that figure is projected to rise as more and more employers choose this cost-effective, less complex alternative to a traditional 401(k).

The benefits of a PEP

PEPs were designed to help eliminate the administrative burden, expense and risk of a traditional 401(k).

Time savings: A Pooled Plan Provider (PPP) handles much of the plan administration, while an

investment manager takes discretion to select and make periodic changes to the investments in your

plan’s menu.

Risk reduction: A PEP allows employers to transfer most of the administrative and fiduciary

responsibilities of sponsoring a retirement plan to the PPP.

Cost efficiencies: A PEP may introduce cost efficiencies through administrative streamlining and shared audit costs.2

Tax credit opportunities: Startup and contribution credits can help employers reduce costs even more. These include:

- Up to $5,000 annually in startup cost credits for three years3

- An extra $500 credit for automatic enrollment3

- A $1,000 per employee contribution credit for employers with up to 50 employees3

How is a PEP managed?

A number of entities all work together to manage a PEP. They greatly reduce the administrative burden to employers, as well as make sure the plan operates smoothly and remains in compliance with regulations.

- PPP: The PPP has fiduciary responsibility for the overall management of the plan.

- 3(16) plan administrator: The PPP serves as the 3(16) operational fiduciary and is responsible for the day-to-day administration of the plan including eligibility, beneficiary tracking and plan disbursements. The PPP handles the heavy liſting so you can focus on running your business.

- ERISA 3(38) investment manager: An ERISA 3(38) investment manager takes responsibility for choosing and monitoring the investments offered to participants in the plan, reducing risk and streamlining plan oversight.

- Recordkeeper: The recordkeeper is responsible for holding plan assets, keeping track of participant information and providing an easy-to-use website where employees can view and manage their accounts.

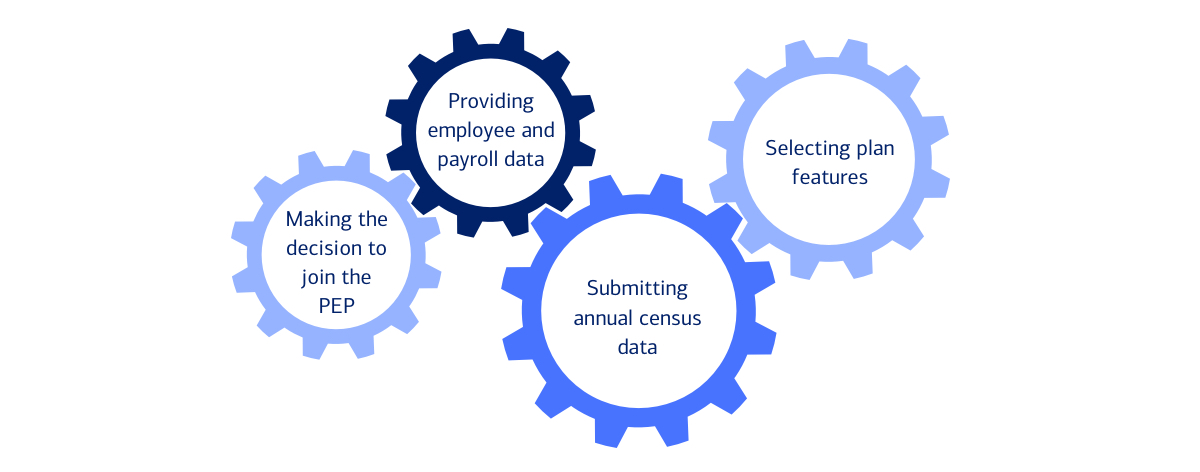

What employers still need to do

Certain responsibilities remain in the hands of employers participating in a PEP. These include:

Who might a PEP be right for?

While businesses of any size can join a PEP, small to mid-size companies that want to sponsor retirement plans for their employees but are concerned about cost, administration and regulatory requirements might find a PEP to be an excellent solution. But it may offer less flexibility and fewer customizable options than standalone 401(k) plans. However, key plan features — like eligibility, matching and vesting — remain in the employer’s control. This can help businesses build a plan that meets their needs while enjoying the benefits that come with a pooled plan.

Key takeaways

- A PEP can help make offering a retirement plan to employees less complicated and potentially more affordable than with a traditional 401(k).

- With a PEP, multiple employers "pool together" to participate in a plan managed by a Pooled Plan Provider (PPP).

- A PEP effectively outsources most of the legal responsibility and administrative burden to entities outside of one's company.

For employers who’ve been reluctant to offer their employees a 401(k) because of concerns about complexity, regulations or administrative burden, the Pooled Employer Plan, or PEP, is something to consider.

1 Cerulli Associates, “PEPs and Participant Personalization Fuel Recordkeeper Growth.”

2 Employers should carefully evaluate the fees and expenses associated with any Pooled Employer Plan before onboarding. PEP costs can vary and employers should compare pricing and features against other available retirement plan solutions to determine the best fit for their company.

3 Retirement Plans Startup Costs Tax Credit. For more information, visit the IRS website, irs.gov/retirement-plans/retirement-plans-startup-costs-tax-credit.